Spring 2026 Housing Market Outlook for Modesto, CA: What Buyers Should Know

Last Updated on May 21, 2026

Preparing for the Spring 2026 Home Buying Season in Modesto

As we move through the spring 2026 home buying season, the Modesto housing market may offer opportunities for buyers who are prepared, informed, and ready to act when the right property becomes available.

Spring often brings more housing activity, including new listings and more buyer interest. For prospective homebuyers in Modesto and the surrounding Central Valley, preparation can make a meaningful difference. Understanding your budget, reviewing your loan options, and getting pre-approved before you begin writing offers can help you shop with greater confidence.

At First Capital Mortgage Inc., we help buyers evaluate mortgage options, understand estimated payments, and prepare for the home buying process. Whether you are a first-time buyer or planning to move up, starting early can help you make better decisions when the right home appears.

- Get pre-approved early: A pre-approval can help you understand your estimated buying power and may strengthen your offer, subject to underwriting, property approval, and program guidelines.

- Understand local trends: Modesto neighborhoods can vary by price range, inventory, property type, and buyer demand. Staying informed helps you make more confident decisions.

- Partner with experienced local professionals: Working with a knowledgeable mortgage broker and real estate agent can help you compare options and avoid unnecessary delays.

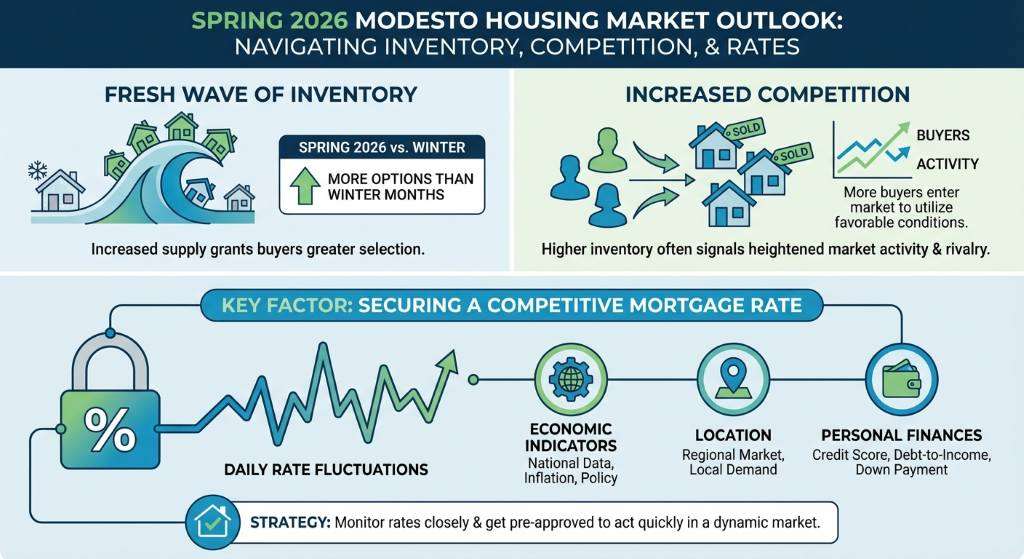

Key Trends Shaping the Modesto Real Estate Market

The spring housing market in Modesto may bring more listings than the slower winter months, but additional inventory can also attract more buyers. Homes that are well-priced, move-in ready, or located in desirable areas may still receive strong attention.

Mortgage rates can change frequently based on inflation, employment data, Federal Reserve policy, bond market activity, and broader economic conditions. Because rates and loan terms vary by borrower profile, property type, occupancy, credit, down payment, and loan program, it is important to review current options before making an offer.

Here are a few practical strategies to keep in mind:

- Compare available loan options: Do not assume one loan program is best for every buyer. FHA, VA, USDA, conventional, jumbo, and other programs may each have different advantages depending on your situation.

- Know your payment comfort zone: The purchase price is only one part of the equation. Taxes, insurance, HOA dues, mortgage insurance, and interest rate all affect the final monthly payment.

- Prepare your documents early: Having income, asset, and credit information reviewed in advance may help reduce delays later in the process.

- Stay flexible: The best opportunity may not be the lowest-priced home. It may be the home that fits your budget, timeline, location needs, and long-term goals.

Modesto Market Snapshot: What Buyers Should Watch

The figures below are provided as general planning examples only. Actual prices, inventory, and days on market can vary by neighborhood, property condition, school district, price range, and current market activity. Buyers should review current MLS data with their real estate professional before making an offer.

| Modesto Area | Buyer Consideration | Market Factor to Watch | Why It Matters |

|---|---|---|---|

| North Modesto | Often popular with move-up buyers | Inventory and pricing by neighborhood | Desirable areas may still attract strong buyer interest |

| Central Modesto | May appeal to buyers seeking established neighborhoods | Property condition and renovation needs | Older homes may require careful review of repairs and costs |

| East Modesto | May offer a mix of price points and home styles | Comparable sales and payment affordability | Payment comfort should be reviewed before writing an offer |

| West Modesto | May appeal to value-focused buyers | Property condition, financing type, and appraisal support | Loan program requirements can affect property eligibility |

How to Prepare for a Modesto Home Purchase Loan

Securing a home purchase loan does not need to feel overwhelming. The key is to start early, understand your options, and work with a team that can help identify potential issues before you are under contract.

At First Capital Mortgage Inc., we guide buyers through the mortgage process by reviewing documentation, comparing available loan programs, and helping clients understand the estimated costs of buying a home.

To begin the pre-approval process, you will typically need to provide:

- Recent pay stubs

- W-2s and/or tax returns, depending on income type

- Bank statements

- Photo identification

- Authorization to review credit

- Information about debts, assets, and employment

Self-employed buyers, investors, and buyers with variable income may need additional documentation. Starting early gives you more time to review options and address questions before making an offer.

Why Pre-Approval Matters Before You Start House Hunting

A mortgage pre-approval can help you understand what you may qualify for before you begin touring homes. It can also help your real estate agent structure a more informed offer when you find a property you want to pursue.

It is important to understand that a pre-approval is not a final loan approval or a commitment to lend. Final approval is subject to full underwriting, appraisal, title review, property eligibility, credit approval, and applicable loan program requirements.

Even with those conditions, pre-approval can be a powerful planning tool. It helps you identify your estimated price range, review potential monthly payments, and prepare for the financial side of buying a home.

Frequently Asked Questions

Q1: Is spring 2026 a good time to buy a home in Modesto, CA?

Spring can be a good time to shop because more homes may come on the market compared with slower seasonal periods. Whether it is the right time for you depends on your budget, payment comfort, loan options, and personal goals.

Q2: How long does it take to close a home loan?

Closing timelines vary based on the loan program, appraisal timing, title work, borrower documentation, underwriting conditions, and property details. Being prepared early may help the process move more efficiently, but no specific closing timeline is guaranteed.

Q3: Why should I get pre-approved before house hunting?

Getting pre-approved can help you understand your estimated buying power and may make your offer more attractive to sellers. It also gives you time to address documentation, credit, or income questions before you are under contract.

Q4: Can I compare mortgage options before committing?

Yes. Reviewing different mortgage options before making an offer can help you better understand estimated payments, closing costs, down payment requirements, and program differences. Available terms depend on borrower qualifications and current market conditions.

Q5: What areas of Modesto are best for first-time buyers?

The best area depends on your budget, lifestyle, commute, property needs, and long-term goals. Central Modesto, West Modesto, East Modesto, and North Modesto may each offer different opportunities depending on current inventory and price range.

Start Your Home Buying Plan Today

If you are thinking about buying a home in Modesto or the surrounding Central Valley, the best first step is to understand your financing options before you begin making offers.

At First Capital Mortgage Inc., we can help you review your loan options, estimate your buying power, and prepare for the spring 2026 housing market with greater confidence.

Ready to take the next step? Contact Steve McNeal and the First Capital Mortgage Inc. team to start your pre-approval review.

Start Your Pre-Approval Review

Phone: 209-522-7100

Email: steve@firstcapitalmortgageinc.com

Compliance Disclaimer: Pre-approval is not a commitment to lend. All loan applications are subject to credit approval, underwriting review, property approval, appraisal, title review, and applicable loan program guidelines. Not all applicants will qualify. Rates, terms, programs, and availability are subject to change without notice. Any market commentary or housing outlook information is provided for general informational purposes only and is not a guarantee of future market conditions, rates, home prices, inventory, or loan approval. First Capital Mortgage Inc. NMLS 2228346. Equal Housing Opportunity.