Down Payment Options in 2026: How Much Do You Really Need to Buy a Home in Modesto?

Last Updated on May 21, 2026

The 20 Percent Down Payment Myth

If you are planning to buy a home in Modesto, California, one of the first questions you may have is: how much money do I really need for a down payment?

Many buyers still believe they need 20 percent down to qualify for a mortgage. While a larger down payment may reduce your monthly payment and may help you avoid mortgage insurance in some cases, it is not required for every buyer or every loan program.

In 2026, many qualified homebuyers may have access to loan programs with lower down payment options. The right program depends on several factors, including credit profile, income, debt-to-income ratio, occupancy, property type, loan amount, location, and program guidelines.

At First Capital Mortgage Inc., we help buyers in Modesto and throughout the Central Valley review available mortgage options so they can better understand their estimated down payment, monthly payment, and cash needed to close.

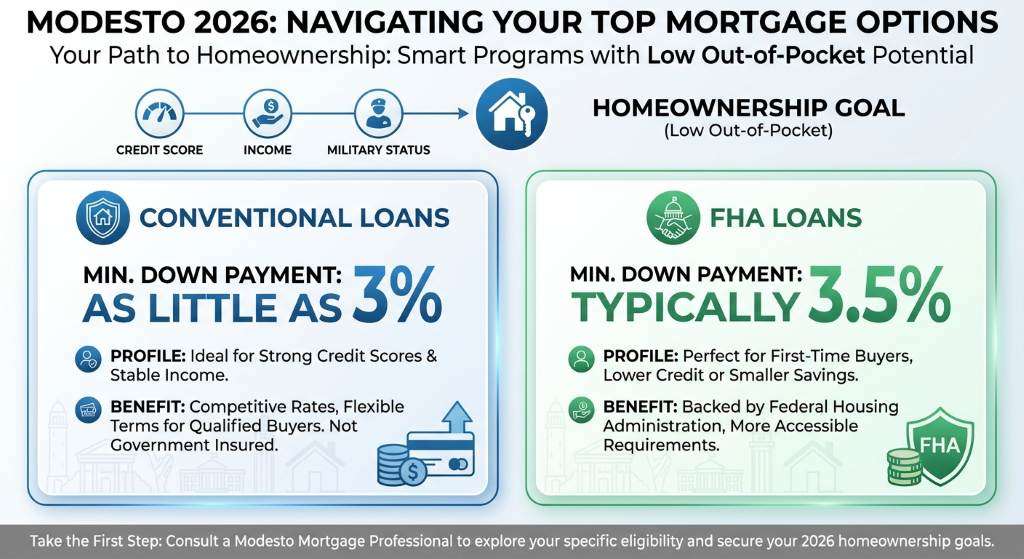

Popular Low Down Payment Options for 2026

Understanding your loan options is an important first step toward homeownership. Depending on your qualifications and the property you are purchasing, you may be eligible for a mortgage program that requires less than 20 percent down.

Here are several common loan options buyers may want to review:

- Conventional Loans: Some conventional loan programs may allow qualified buyers to purchase with as little as 3 percent down. Eligibility depends on credit, income, occupancy, property type, loan limits, and underwriting guidelines.

- FHA Loans: FHA loans may allow eligible buyers to purchase with as little as 3.5 percent down. FHA financing can be helpful for some first-time buyers and buyers who need more flexible credit guidelines, subject to program requirements.

- VA Loans: VA loans may offer eligible veterans, active-duty service members, and certain surviving spouses a zero-down-payment option. VA eligibility, entitlement, property approval, and lender guidelines apply.

- USDA Loans: USDA loans may offer zero-down-payment financing for eligible buyers purchasing eligible properties in qualifying rural or certain suburban areas. Income limits, location eligibility, and program guidelines apply.

When you work with an experienced mortgage broker, you can compare multiple loan options and determine which programs may fit your financial goals. No single loan program is right for every buyer, which is why reviewing the full picture matters.

Common Down Payment Options by Loan Type

The table below provides general information about common minimum down payment options. Actual eligibility depends on borrower qualifications, property details, loan limits, occupancy, and current program guidelines.

| Loan Type | Possible Minimum Down Payment | May Be a Fit For |

|---|---|---|

| Conventional Loan | As low as 3% for certain qualified buyers | Buyers with qualifying credit, income, and debt-to-income ratios |

| FHA Loan | As low as 3.5% for eligible buyers | Buyers who may benefit from more flexible credit or qualification guidelines |

| VA Loan | 0% down may be available | Eligible veterans, active-duty service members, and certain surviving spouses |

| USDA Loan | 0% down may be available | Eligible buyers purchasing eligible properties in qualifying locations |

How to Prepare Your Finances for a 2026 Home Purchase

Once you understand that 20 percent down is not always required, the next step is preparing your finances. Starting early can help you identify the right loan path and avoid surprises when you are ready to make an offer.

Here are a few practical steps to consider:

- Review your credit: Your credit profile can affect your available loan options, interest rate, mortgage insurance, and overall qualification.

- Estimate your full cash needed to close: Your down payment is only one part of the cost. Buyers should also plan for closing costs, prepaid taxes and insurance, inspections, appraisal fees, and other transaction-related expenses.

- Get pre-approved early: A pre-approval can help you understand your estimated buying power and may strengthen your offer, subject to underwriting, property approval, and program guidelines.

- Compare loan programs: FHA, VA, USDA, conventional, jumbo, and other programs may have different down payment requirements, mortgage insurance rules, and qualification standards.

- Understand payment comfort: The lowest down payment option is not always the best option. It is important to review your estimated monthly payment, total cash needed, and long-term financial goals.

If you are thinking about buying a home in Modesto, Steve McNeal and the team at First Capital Mortgage Inc. can help you review available loan options and prepare for the next step. Closing timelines vary based on the loan program, appraisal timing, title work, underwriting conditions, property details, and borrower responsiveness.

Can You Use Gift Funds for a Down Payment?

Many mortgage programs may allow gift funds from an eligible donor, but the rules vary by loan type. In many cases, the lender will need documentation showing where the gift funds came from, who provided them, and that repayment is not expected.

Gift funds may be helpful for qualified buyers who have the income to afford the home but need assistance with the down payment or closing costs. Before relying on gift money, it is important to review the requirements for your specific loan program.

What About Mortgage Insurance?

If you put less than 20 percent down on a conventional loan, private mortgage insurance, often called PMI, may be required. PMI requirements, costs, and cancellation rules vary based on the loan program, loan-to-value ratio, credit profile, and lender guidelines.

FHA loans use mortgage insurance premiums, which are different from conventional PMI. VA loans do not have monthly mortgage insurance, but they may include a VA funding fee unless the borrower is exempt. USDA loans may include guarantee fees. These costs should be reviewed carefully when comparing programs.

Frequently Asked Questions

Q1: What is the minimum down payment needed to buy a house in California?

The minimum down payment depends on the loan program and borrower eligibility. Some qualified buyers may be eligible for 0 percent down through VA or USDA financing, while certain conventional programs may allow as little as 3 percent down. FHA loans may allow as little as 3.5 percent down for eligible borrowers.

Q2: Do I have to pay private mortgage insurance if I put less than 20 percent down?

For many conventional loans, PMI may be required when the down payment is less than 20 percent. FHA, VA, and USDA loans have different insurance or guarantee fee structures. The right comparison depends on your loan type, credit profile, down payment, and long-term goals.

Q3: Can I use gift money for my down payment?

Many loan programs allow gift funds from eligible donors, but documentation is required and rules vary by program. Before using gift funds, it is best to confirm the guidelines for your specific loan option.

Q4: How do I know which mortgage loan is right for me?

The best loan depends on your credit, income, assets, debts, down payment, property type, occupancy, and long-term financial goals. A mortgage review can help compare your options side by side so you can make an informed decision.

Q5: How fast can I get pre-approved for a home loan in Modesto?

Pre-approval timing depends on how quickly your application and supporting documents are submitted and reviewed. Starting early can help you understand your options before you begin writing offers.

Start Your Down Payment Conversation Today

You may not need 20 percent down to buy a home in Modesto. The right strategy depends on your qualifications, available loan programs, monthly payment goals, and how much cash you want to keep in reserve after closing.

At First Capital Mortgage Inc., we can help you compare down payment options, estimate cash needed to close, and prepare for your home purchase with greater confidence.

Ready to review your options? Start your pre-approval review today and find out which mortgage programs may fit your goals.

Start Your Pre-Approval Review

Phone: 209-522-7100

Email: steve@firstcapitalmortgageinc.com

Compliance Disclaimer: Pre-approval is not a commitment to lend. All loan applications are subject to credit approval, underwriting review, property approval, appraisal, title review, and applicable loan program guidelines. Not all applicants will qualify. Rates, terms, programs, fees, down payment requirements, mortgage insurance, and availability are subject to change without notice. VA, USDA, FHA, and conventional loan program eligibility requirements apply. Any examples are provided for general informational purposes only and are not a guarantee of loan approval, interest rate, payment amount, or program availability. First Capital Mortgage Inc. NMLS 2228346. Equal Housing Opportunity.